Consumer Duty: What changes can customers expect in financial services?

User Experience & Usability

Overview

If you don’t work in the financial sector, you may have missed the new rules and guidance from the Financial Conduct Authority (FCA) on Consumer Duty (FG22/5), which take effect for financial products and services on sale or up for renewal, on 31st July 2023.

It’s no secret that many consumers have built up a negative perception of banks due to closing branches, no loyalty rewards, poor customer service – the list goes on. The Duty aims to initiate a shift towards positive customer outcomes, by asking businesses to put user needs at the heart of their culture, and sets higher standards of care to avoid foreseeable harm and support people’s financial objectives.

Sounds great right?! But what tangible differences should customers be expecting to experience over the coming months?

1. Less complexity & informed decision-making

The FCA recognises that customers are only able to make effective decisions in line with their interests when they are offered clear and honest information, and that frankly this often isn’t the case. To support this, and address fading confidence in financial services, ‘Consumer understanding’ is one of four key areas where businesses must take further responsibility.

This will result in the following experiences:

Where complex information is present in a user journey – think, for example, about the terms & conditions for an insurance policy – customers should no longer be directed to a 200-page PDF with a single wall of text. Guidance suggests layering information, whereby key elements are explained upfront, with clear signposting and cross-references to further detail. This will prevent people from overlooking important information such as claim terms, which are often hidden away.

Customers should receive communications that are engaging, logical and succinct. For example, if an account benefit (e.g. 0% interest on a Credit Card) is coming to an end, your bank must make you aware of this, with an appropriate level of information, and allowing sufficient time for you to consider your options. Providers should help rather than hinder customers in making the right choice for their circumstances.

Friction will only be used positively, to protect people from actions that may result in avoidable harm. So, whilst features like gambling blocks will stay, it should become easier for customers to switch or exit products, without the rigour of having to call customer services and be subjected to a 30-minute conversation trying to persuade you otherwise. As a result, we should see streamlined user journeys that don’t cost as much time and effort.

2. Better overall value

The guidance explains that the value offered to customers is comprised of both monetary and non-monetary costs towards a product or service. Whilst reinforcing the need to deliver high quality experiences, new rules also require companies to assess whether prices paid by the customer are reasonable given the benefits (and limitations) that they will receive.

In practice, this will mean:

Information should be transparent during the sales process, so that customers can easily evaluate the value of something compared to other options, as well as their financial objectives. Companies are no longer allowed to deliberately make this difficult and must avoid dark patterns such as misdirection to distract from important terms, or having a complex pricing structure that is difficult to compare.

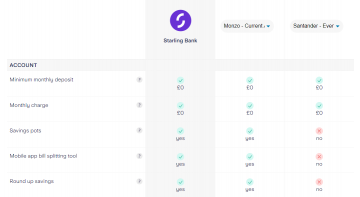

Table to ‘Compare current accounts’ on the Starling Bank website

The financial cost of products and services, including additional fees, will become fairer, and align with what is being provided. For example, the cost for changing your address or exiting a contract will now reflect underlying administrative charges, rather than providers being able to add what they like on top.

Vulnerable customers, who due to personal circumstances are especially susceptible to harm, should be better protected as providers must consider how to deliver fair value to different user groups. In addition to ensuring all costs are understood upfront, the impact of unplanned occurrences such as late payment charges should be better recognised and addressed, to prevent foreseeable harm like spiralling debt.

3. Positive customer support

Central to the rules and guidance is a new consumer principle requiring businesses to ‘act to deliver good outcomes for retail customers’ throughout each user journey. This requires them to prioritise customer needs above financial gains, and we expect user research to be integral to building a detailed understanding of consumer behaviour. One of the areas where companies are required to implement learnings and good outcomes is customer support.

Here are some of the changes we anticipate:

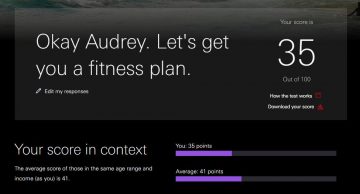

Customers should be empowered to maximise the benefits they receive from financial products and services that have been designed with them in mind, as providers support them in understanding and using these throughout their lifecycle. For example, we should see companies directing individuals to products and features that will help them achieve financial goals such as saving.

Example output from HSBC’s Financial Fitness Checker

Increased visibility, a choice of channels, and intuitive navigation should make the act of getting support easier for customers. For example, those who find it difficult to relay or process verbal information should be able to get written support within a comparable timeframe, and with equal expertise.

Overall, changes should result in higher levels of satisfaction amongst customers, and a positive ongoing relationship with their providers. In line with the Duty, people can expect queries to be addressed with reasonableness, with handlers paying increased attention to and better educated on vulnerabilities, and the impact that decisions will have on the individual customer. Companies will also have a responsibility to signpost people to external support when they are unable to provide relevant guidance or access to products.

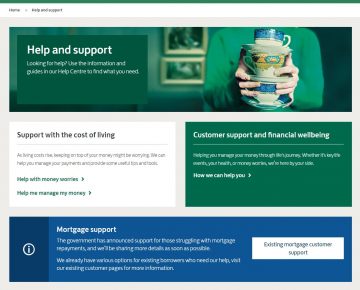

Help and support page on the Lloyds Bank website

4. Ongoing improvements & accountability

To drive genuine change within the financial sector, the Consumer Duty has put processes in place to hold companies accountable for the experiences they offer. Once customer needs have been identified, providers must test and monitor real-life outcomes, identifying where these fall short of compliance and/or improvements can be made. There is an expectation for this to become embedded across functions from product development to servicing, with seniors in each business championing a customer-centric approach and signing off an assessment at least annually.

The impact?

Whilst we aren’t going to see customer frustrations disappear overnight, we are confident in seeing gradual improvements in line with the four key areas in the Duty; products and services, price and value, consumer understanding and consumer support. For example, if there are a high number of drop-offs at a specific point in the customer support process (e.g. when phone calls are being transferred), there is now an obligation for this to be recognised and resolved.

Customers should start to feel more valued, protected and supported by financial providers, at every stage of the user journey. Where problems do arise, these should be identified and addressed quickly, and less individuals should fall into financial difficulty as a result of foreseeable events.

Overall, we see a positive future for the finance industry due to the new Consumer Duty, and strongly agree with the drive to put customers first. Conforming to much of the guidance will rely on collecting information to monitor the outcomes that customers are receiving, and customer research will be an important part of this. Companies will also need to test content such as communications before launch to ensure that it supports understanding and decision-making.

If you need support to take a customer-centric view on your products and experiences to align with the requirements of the Consumer Duty, please get in touch with one of our team. We are already working with clients in this area and would be delighted to support you!

We were approached to review and test an existing application to understand the user journey and discover what were the main pain-points and help to ...

We were approached to review and test an existing application to understand the user journey and discover what were the main pain-points and help to write a brief for a redesign...

Testing your product or service with your users is an invaluable part of the design and development process. It will identify usability problems and ...

Testing your product or service with your users is an invaluable part of the design and development process. It will identify usability problems and highlight ways to improve the users’ experience...